Should I Claim 0 Or 1 If I Am Married? Making Your W-4 Work For You

Deciding how many allowances to claim on your W-4 form when you are married can feel a bit like a puzzle, can't it? This choice directly shapes how much money comes out of your paycheck for taxes, and ultimately, what happens at tax time. For many married couples, especially those where both partners work, figuring out the right number of allowances is a very common question, and getting it right helps you manage your money all year long.

It's a really important decision, because it impacts your immediate take-home pay versus the possibility of a larger refund later. Claiming too few allowances means more money is withheld, which typically leads to a refund. On the other hand, claiming more allowances means you get more money with each paycheck, but you might owe taxes when you file your return. It's about finding that sweet spot for your unique financial picture, you know?

This article will explore the impact of claiming 0 or 1 on your tax withholding as a married individual. We'll look at different scenarios, like when both partners earn money, and help you learn how to adjust your allowances for your own financial goals. So, let's figure this out together, shall we?

Table of Contents

- Understanding Tax Allowances: The Basics

- Married and Working: The Dual-Income Dilemma

- Finding Your Sweet Spot: Practical Advice

- Special Situations and Important Notes

- Beyond Allowances: Other Factors

- People Also Ask

Understanding Tax Allowances: The Basics

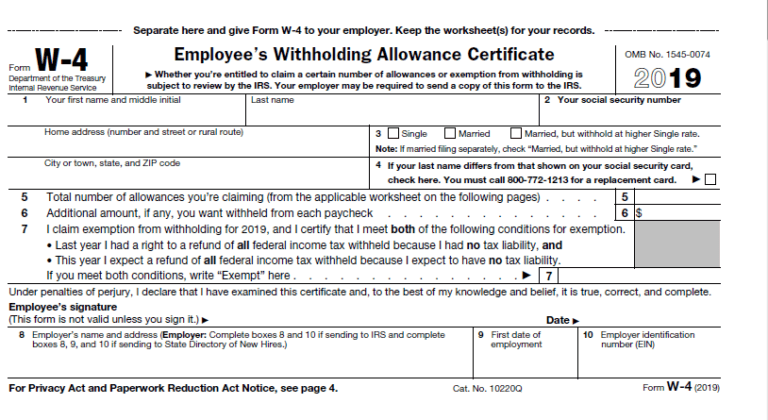

When you fill out your W-4 form, you're telling your employer how much federal income tax to hold back from your pay. The number of allowances you claim helps determine this amount. It's a system designed to get you close to paying the right amount of tax throughout the year, so you don't have a huge surprise at tax time. This can be a bit difficult to grasp at first, but it's really about matching your withholding to your expected tax bill.

What "Claiming 0" Really Means

Claiming 0 allowances means your employer will hold back the most amount of tax possible from each paycheck. This choice often gives the impression that the person with the income is the only earner in the family, or that they want to be very cautious with their tax payments. It means less take-home pay for you right now, but it also increases the chance of getting a bigger tax refund when tax season rolls around. So, if you like the idea of a larger lump sum back from the government, claiming 0 might be a good fit for you.

It's basically like giving the government an interest-free loan throughout the year. For some people, that's a good way to save money without really thinking about it. For others, they might prefer to have that money in their pocket right away. It's a personal choice, of course, and depends on your spending habits and financial plan. Claiming zero allowances is a very conservative approach to tax withholding, and it's almost surely what is happening on your return if you find yourself getting a large refund each year, especially if you do not have access to many credits and deductions.

The Impact of "Claiming 1"

Claiming 1 allowance means your employer will hold back less tax from each of your paychecks compared to claiming 0. This gives you more money in each paycheck, which can be very appealing for day-to-day budgeting. However, it also means you might get a smaller refund at tax time, or even owe money if not enough tax was held back. A married couple with no children can claim 1 allowance each, which is a common setup for many households.

For a single person with just one job, claiming 1 allowance is typically a good idea. It often leads to a balanced outcome where you're not overpaying too much, and you're not underpaying either. You should claim 1 allowance if you are married and filing jointly, as this is a general guideline for many couples. This approach usually means you will likely be getting a refund back come tax time, but it might not be as big as if you claimed 0. It's all about balancing that immediate cash flow with your tax obligations, you know?

Married and Working: The Dual-Income Dilemma

When both partners in a marriage are working, the tax situation becomes a bit more nuanced. The W-4 system, especially before recent updates, sometimes assumed only one income per household when you selected "Married Filing Jointly." This can lead to less tax being withheld than needed, particularly if both incomes together push you into a higher tax bracket. It's a common scenario, and many couples face this very challenge.

When Both Claim Zero

If both you and your spouse are claiming "Married" and "0" allowances on your respective W-4 forms, you might think you're being extra careful and ensuring enough tax is held back. However, this is almost surely what is happening on your return if you end up owing taxes, especially if you do not have access to many tax credits and deductions. The system might not account for your combined income effectively, meaning that even with both claiming 0, you could still underpay.

This happens because each employer withholds tax based on the assumption that their employee's income is the primary or sole income for a household of their filing status. When you combine two incomes, the total amount can jump into a higher tax bracket than either individual income would suggest. So, while claiming zero individually seems safe, it can actually lead to an unexpected tax bill for the couple, which is, well, not ideal.

The 25% Tax Bracket Consideration

A significant point to consider is what happens if both of you earn an income and your combined earnings reach the 25% tax bracket or higher. In such cases, it's very possible that not enough tax is remitted when your incomes are combined, even if you both claim 0 allowances. The tax withholding tables are set up so that each job withholds tax as if it's the only source of income for a married couple. When you add another income, the total amount of income that is taxed at a lower rate is essentially doubled, but the total tax due is calculated on the combined higher income.

This means that the total amount withheld from both paychecks might not be enough to cover the actual tax liability for your combined income. More of what you earn will be subject to higher tax rates than what your individual W-4s account for. It's a common reason why dual-income couples sometimes find themselves owing money at tax time, and it's a good reason to look closely at your withholding strategy.

Finding Your Sweet Spot: Practical Advice

The decision of whether you or your spouse should claim 1 or 0 allowances, or some other number, truly depends on your specific financial situation. There isn't a single answer that fits everyone. The goal is to get your withholding as close as possible to your actual tax liability, avoiding a huge refund (which means you overpaid) or a big tax bill (which means you underpaid). It's a balancing act, you know?

Claiming 1 Each: When It Works

For many married couples filing jointly, claiming 1 allowance each can be a good starting point. This is often recommended as a general guideline. If you are filing as the head of the household, then you would also claim 1 allowance. This approach typically aims to balance your take-home pay with your tax obligations, meaning you will likely be getting a refund back come tax time, but it might not be a very large one. It's a rather straightforward approach for couples with fairly stable incomes.

However, as mentioned, if both of you earn a significant income and your combined earnings reach higher tax brackets, claiming 1 each might still not be enough to prevent owing taxes. It's a good baseline, but it's not a one-size-fits-all solution, particularly for higher-earning couples. You might need to adjust further, perhaps by having one person claim 0, or by using the "Married, but withhold at higher single rate" option on the W-4, which is a bit more aggressive.

Adjusting for Your Financial Goals

Explore the impact of claiming 0 or 1 on your tax withholding as a married individual and learn how to adjust it for your financial goals. If you prefer more money in each paycheck to help with current expenses or to invest, you might lean towards claiming more allowances (like 1 each). This gives you more immediate cash flow. But if you prefer a larger tax refund as a kind of forced savings, then claiming fewer allowances (like 0) would be more suitable. It's really about what works best for your household's budget and saving habits.

Some people like the discipline of a larger refund, using it for a big purchase or to pay down debt. Others find it more beneficial to have that money throughout the year, earning interest or just making daily life a little easier. Your decision should align with your personal financial strategy for the year. This can be a difficult decision, but looking at your budget and future plans can help.

Considering Credits and Deductions

Your access to various tax credits and deductions also plays a big role in how many allowances you should claim. If you expect to qualify for significant credits, like the Child Tax Credit or education credits, you might be able to claim more allowances without owing money, because those credits directly reduce your tax bill. On the other hand, if you don't have many deductions or credits, you'll need to be more careful with your allowances to avoid an unexpected tax bill. So, basically, it's about looking at your whole tax picture.

For instance, if you have children, you might be able to adjust your allowances to account for the Child Tax Credit. This would first ask you to consider how many qualifying children you have. It's about being proactive and estimating your tax situation as best as you can. You don't want to pay owe taxes, but you also don't want to give the government an interest-free loan all year. It's a rather delicate balance.

Special Situations and Important Notes

There are a few particular situations that can change how you should approach your W-4 allowances. It's important to consider these unique circumstances to make sure your withholding is as accurate as possible. These situations can sometimes lead to unexpected outcomes if not handled properly, so it's good to be aware.

If Someone Claims You as a Dependent

You should note that if someone else mentions you as a dependent on their tax return, you will not get any allowances for yourself. This is a pretty straightforward rule. If your parents, for example, claim you as a dependent, then your own W-4 form would typically show 0 allowances, regardless of your marital status or income. This is because the tax benefit of your dependency is being claimed by another taxpayer.

This rule helps prevent double-dipping on tax benefits. It ensures that the tax system accounts for your financial support being provided by another person or family unit. So, if you're a young adult who is still financially supported by your parents, even if you're married, this is a very important point to remember when filling out your W-4.

The W4 Worksheet: Your Best Friend

The W-4 form includes a worksheet specifically designed to calculate the total number of allowances you should claim across all your jobs and your spouse’s jobs. This worksheet is an incredibly helpful tool for married couples, especially those with multiple incomes. It guides you through a series of questions to help you arrive at a more accurate number for your household's total allowances. Typically, it’s best to claim all the allowances that the worksheet suggests to get your withholding as close as possible to your actual tax liability.

Using this worksheet can prevent situations where you might owe taxes because of insufficient withholding, particularly if you're both working. It helps you account for the combined effect of your incomes and any credits or deductions you expect to take. It's a really good idea to revisit this worksheet any time your financial situation changes, such as getting a raise, changing jobs, or having a child. You can find this worksheet on the IRS website, and it's a great resource to learn more about tax withholding.

Higher Single Rate for Lower Earner

For married couples where both partners work, a common strategy to avoid owing taxes is for the lower wage earner to claim "Married, but withhold at higher single rate" and zero allowances on line 5 of their W-4. This option causes more tax to be withheld from that individual's paycheck, helping to compensate for the potential under-withholding that can occur when two incomes are combined. I highly recommend this approach if you are the lower wage earner and you don't want to owe taxes at the end of the year.

This method helps ensure that enough tax is held back from your combined income, especially if both of you earn an income and it reaches the 25% tax bracket or higher. It's a proactive way to manage your tax payments throughout the year, aiming for a smaller refund or a zero balance rather than an unexpected tax bill. It's a very effective strategy for many dual-income households to prevent tax surprises.

Beyond Allowances: Other Factors

While allowances are a big part of your W-4, other life changes can also affect your tax situation. Keeping up with these changes is important for accurate tax planning throughout the year. It's not just about the numbers you put down, but also about staying informed.

Reporting Changes (Marriage, PTC)

If one or both of you are receiving advance payments of the Premium Tax Credit (PTC) and you have a change in circumstances, like getting married, you should promptly report it to your Health Insurance Marketplace. Getting married changes your household size and income, which can affect your eligibility for and the amount of the PTC. Failing to report these changes could mean you receive too much or too little credit, leading to adjustments when you file your taxes. This is a very important step to take.

It's about keeping your tax situation current with life events. Marriage is a significant life change that impacts many areas of your finances, including your taxes and any advance credits you might be receiving. Being proactive about reporting these changes helps you avoid unexpected tax consequences later on. To learn more about tax implications of life events, you can visit our site.

People Also Ask

Here are some common questions people have about claiming allowances when married:

What happens if both married individuals claim 0?

If both married individuals claim 0 allowances, it means the maximum amount of tax is withheld from each of their paychecks. While this might seem like a safe bet to avoid owing money, if both of you earn a good income and your combined earnings reach higher tax brackets, it's almost surely what is happening on your return if you still end up owing taxes. This is because the withholding system often assumes each job is the primary income for a married household, not accounting for the combined effect of two incomes pushing you into a higher tax bracket.

Does claiming 1 allowance mean more money in my paycheck?

Yes, claiming 1 allowance typically means that less tax will be withheld from your paycheck compared to claiming 0 allowances. This results in more take-home pay with each paycheck. While this gives you more immediate cash, it could also lead to a smaller tax refund at the end of the year, or even mean you owe taxes if not enough was withheld for your overall tax liability, especially if you have other income sources or your spouse also works.

Can a married couple with no children claim 1 allowance each?

Yes, a married couple with no children can claim 1 allowance each. This is a common and often recommended approach for many married couples filing jointly. It generally aims to strike a balance between your take-home pay and your tax obligations, often resulting in a modest refund at tax time. However, if both spouses earn a significant income, they may need to adjust their withholding further (perhaps by one claiming 0 or using the "Married, but withhold at higher single rate" option) to avoid owing taxes.

Should I Claim 1 or 0 on My W-4 Allowances? (2025)

Should I Claim 0 or 1 on W-4? 2024 W-4 Expert's Answer!

Understanding Tax Exemptions: Should You Claim 0 or 1?